When investing in property you have most likely heard the saying ‘it’s not the TIMING OF THE MARKET – it’s the TIME IN THE MARKET’ that is important. For long term ‘set and forget’ investors, this is an appropriate comment. However, one of the most important keys to success with property investment is also KNOWING WHEN the market presents great opportunities. When to get in, when to get out, when to wait and when to hold…

So how do you identify good investment opportunities?

Although there are some historical signs and patterns for property investors to work with, in more recent times regulation and the political environment have certainly changed the playing field in the world of property investment.

There are a number of factors that come into play and provide us with hints including:

1. housing availability

2. interest rates and finance trends

3. borrowing capacity and debt serviceability levels

1. Housing availability

During a property boom, auction

clearance rates consistently top 75%1 with properties staying on the market for ridiculously short periods. Many of these properties do not even make it to open house or auction day. This is what we see in the below graph from mid 2014 until about mid 2017. These are clear signs of being at the higher end of a property market.

What we need to look for in a buyers’ market is a slowing down with a reduction of properties on the market and lower auction clearance rates.

In the first few months of this year, we saw clearance rates averaging around the 44% mark nationally, ending the first quarter at around 56.8% (started to increase just before Easter).

Comparative to the last 12 months, there is a decrease of new properties in the market, however the total number of properties for sale nationally is higher.

This indicates that the market is now holding more properties as it is taking longer for vendors to sell with the possibility of having to offer significant reductions in order to move their property.

In summary – what does this mean?

• More houses in the market than buyers

• Longer timeframe to sell

• Buyers taking their time to purchase

• Vendors potentially having to reconsider their asking price

These can be signs of reaching or approaching the bottom of the property market and introducing a property buyers’ market.

Because of the reduction in housing prices, a property that may have been unattainable for you 12-18 months ago may now be within your grasp.

Another sign that we could be entering a buyers’ market is when rental yields start to increase. When this happens, it is a sign that people are now putting their property search on hold for a while, they continue to rent or our potential first home buyers are entering the rental market for the first time.

The first CoreLogic Quarterly Rental Review for 2019 showed that national weekly rents have risen by 1% during the first three months of the year.

2. Interest rates and finance

trends

Historically, property cycles have been dictated by the changes in interest rates but the RBA has been holding the cash rate at a record low for nearly three years now.

The current downturn in lending has also been influenced by credit availability. This was apparent during the Banking Royal Commission with lenders tightening their criteria and APRA capping interest only loans (typically used by investors).

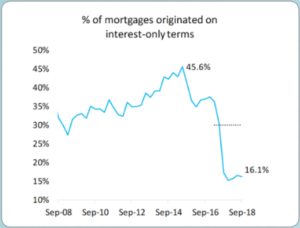

For the first time in history many home owners have been tapping into interest only loans as well as investors, bringing an all-time high in interest only loans of 45.6% in 2015 as a proportion of total borrowings as seen below. This also had an impact on investor borrowing as indicated in both charts.

However in December 2018 we saw the restriction being lifted on interest only loans.

Is this a sign that they want investors back in the market?

It is also important to note that although the RBA has held the cash rate steady, variable mortgage rates have crept up over the last 12 months with the major banks independently of any official cash rate movement. The lenders are taking it into their own hands to increase rates. And when one major lifts rates, the others follow.

The good news is…

Due to the greater competition from second tier lenders and non-bank lenders, there are still very competitive rates available for buyers through mortgage brokers.

We have access to many alternate lenders outside the majors so you can trust that we will be considering these options when assessing your finance opportunities.

3. Debt serviceability

It could be argued that the amount of debt we have is not the issue. Instead, it’s the serviceability of that debt. Australian debt as a total has grown, but the interest paid on that debt (as a percentage of household disposable income) has fallen.

Interest paid on those increased levels of debt has stayed relatively manageable because interest rates have remained low.

The concern we all have when it comes to servicing our debt is the potential for personal circumstances to change.

Good debt can turn to bad debt very quickly when a property loses value instead of gaining value or when personal circumstances change (eg divorce, redundancy or illness). These events can make your loan repayments become unmanageable.

If you find yourself in this situation, early action is the best move forward.

In summary…

As for that ticking property time bomb, it could be said it’s more of a property clock, and understanding how to read the property cycle clock plays a large role in weighing up risk and your investment strategy.

Finally, we are yet to fully understand how the outcome of the federal election will play out for the finance and property market and the recommendations from the Banking Royal Commission being implemented or not. So stay tuned for updates as they progress with these decisions.

In the meantime, if you want to take advantage of the potential buyers’ market – we look forward to your call.